For several years now, with technological and legal hurdles getting smaller, many industry segments have developed a much more “user-friendly” and efficient setup. Lodging elsewhere has become much easier thanks to Airbnb*1), advertising no longer needs a media agency thanks to digital ads, and everybody has access to the latest music with Spotify*2) on their smartphone.

All these “disruptions” followed a very similar pattern: from a starting point of “friction” and limited alternatives, to a phase when “friction-less” business is proven as new technologies and business models emerge, to a final phase with established new business models and new profit distribution.

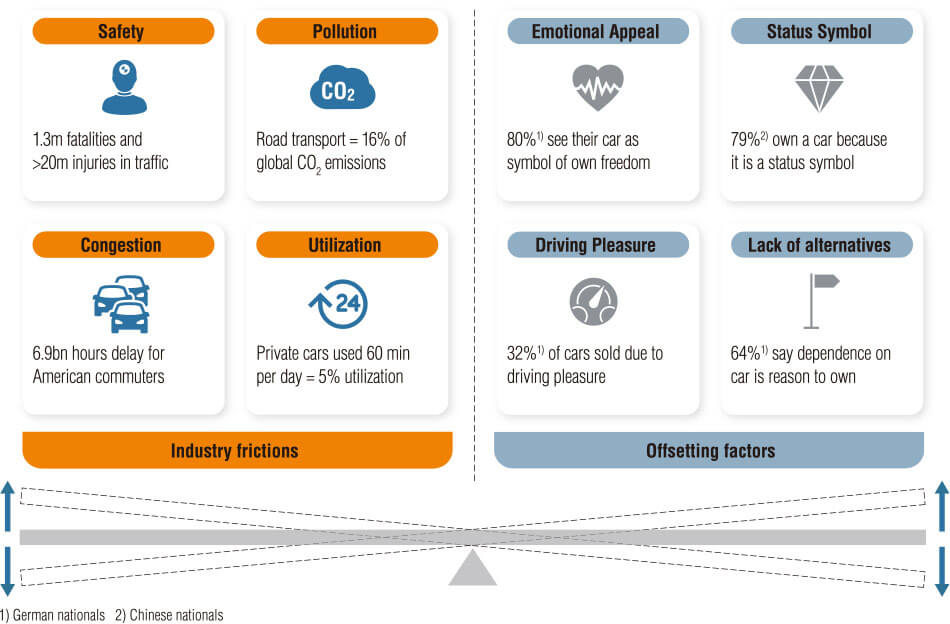

The automotive industry is one of the few exceptions. For a long time, it succeeded in maintaining a highly inefficient status though there was no lack of pain points: safety, pollution, or congestion, just to mention a few. It managed to do so by positively addressing customer emotions – the emotional appeal of cars – its function as status symbol or just a lack of alternatives (see Figure 1).

However, many existing hurdles to a “lower friction segment” have started to shrink, creating the basis for real disruption now.

Figure 1 - System Friction and Industry Approach to Offset  The Automotive industry was able to maintain a highly inefficient status by positively addressing customer emotions - but how long?

The Automotive industry was able to maintain a highly inefficient status by positively addressing customer emotions - but how long?

- *1)

- Airbnb is a registered trademark of Airbnb, Inc. in the US and abroad.

- *2)

- Spotify is a registered trademark of Spotify AB.

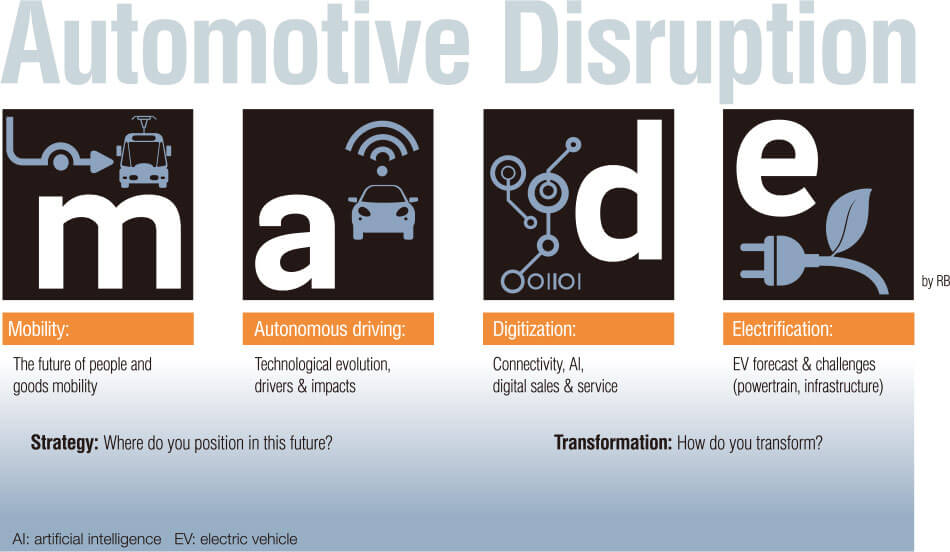

These four trends drive disruption of mass and individual mobility:

Out of the current automotive disruptive trends there are four major elements that will determine the automotive industry “end game.” These are reflected in the Roland Berger 2017 Automotive Global Campaign “MADE by RB” (see Figure 2):

Figure 2 - Automotive Disruption  The figure shows the four key trends that will determine the automotive industry.

The figure shows the four key trends that will determine the automotive industry.

Mobility:

New players like Uber*3) push and break conventions. Established original equipment manufacturers (OEMs) enter new mobility businesses. Cities push for new mobility concepts.

- *3)

- Uber is a trademark and brand of Uber Technologies, Inc.

Autonomous driving (AD):

Arrives ahead of schedule and a lot of new entrants and real-life pilots are already under way. We observe enormous technological progress in AD systems and strongly increasing R&D funding. Even the legislative framework develops quicker than some could imagine. Real-life robocab tests are already under way.

Digitization:

As the sophistication of digital technologies increases, specific technology thresholds have already been surpassed. Tech giants make strong investments in AI which is able to solve highly complex problems (deep learning).

Electrification:

A radically altered legislative landscape and market upheavals are accelerating powertrain electrification. We see impressive technological progress in batteries on the one hand, reduced credibility and influence of the “old” automotive industry on the other (Dieselgate). OEMs are shifting focus to e-propulsion and try to increase customer pull.

The coincidence of these four trends fuels a potential disruption. Not only for personal mobility, but also goods transportation, raising questions like:

- Will cars still be owned? If yes, how many?

- Will robocabs become a reality?

- How will this affect the automotive industry and especially its relevance as one of the biggest employers worldwide?

- What is the dominant delivery solution for the last mile?

- Will trucks ever drive autonomously without drivers?

There is still a lot of uncertainty on what the end game will look like and, even more so, how the transition towards that end-game might turn out.

The future of mobility:

how much will everything change?

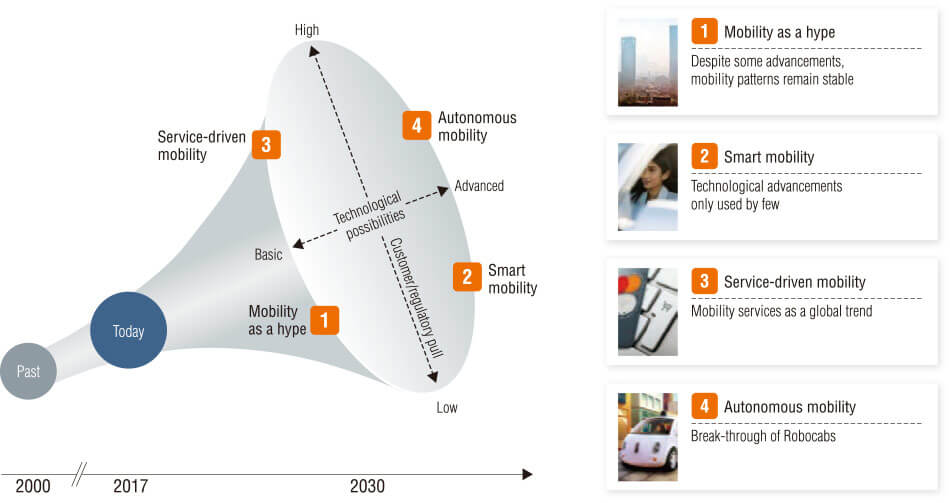

The automotive industry megatrends are expected to evolve along two main angles: technological possibilities as well as customer/regulatory push. For example, increasing emission regulations and rising customer demand can enhance the breakthrough of shared mobility services.

Depending on the speed of technological innovation and the progressiveness of customers and regulators, we see a range of potential 2030 market scenarios that differ by number and types of vehicles, dominant business model, and value chain configuration (see Figure 3).

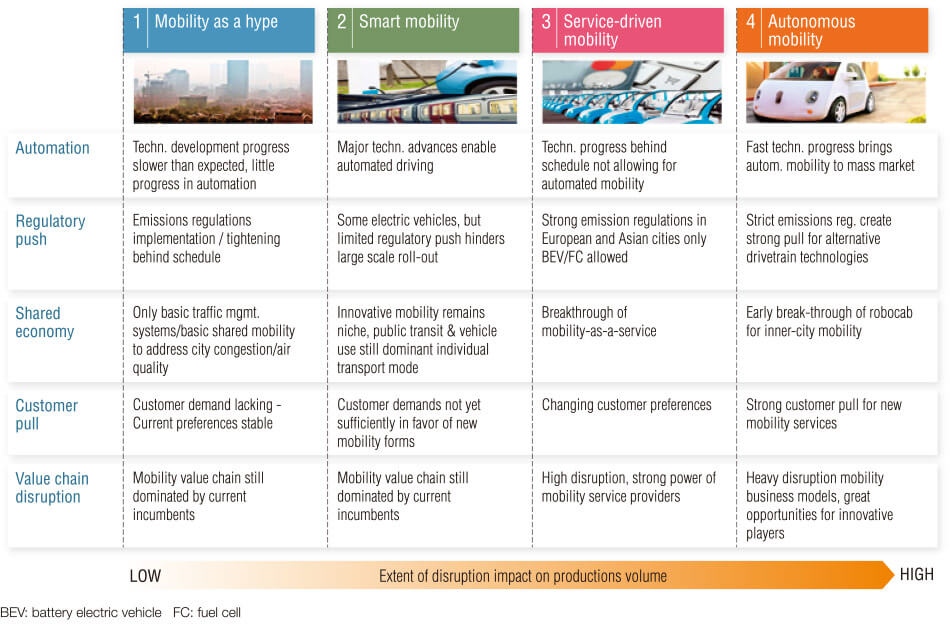

Figure 3 - Overview of Global Mobility Scenarios: Possible Futures 2030  We differentiate four distinct mobility scenarios that differ in their technological state as well as customer acceptance

We differentiate four distinct mobility scenarios that differ in their technological state as well as customer acceptance

In a business-as-usual scenario, technological development and customer respectively regulatory pull progress only slightly. Existing business models stay in place. “Mobility” turns out to be an only temporary hype (see “1 Mobility as a hype” in Figure 4).

The Smart mobility scenario assumes that despite technological advancements mobility does not become a mass-phenomenon as customer demands and regulation are not yet in favor of these developments and hinder large-scale roll-out (see “2 Smart mobility” in Figure 4).

The third scenario sees service-based business models emerge, fueled by changing customer preferences. However, technological progress remains behind schedule not yet allowing for automated mobility solutions (see “3 Service-driven mobility” in Figure 4).

The most radical autonomous mobility scenario forecasts a massive disruption of mass transit and individual mobility by automated mobility solutions due to overwhelming technological progress as well as a high customer acceptance. A high level of digitization would characterize all processes and infrastructures (e.g. digital customer interfaces, traffic management, etc.) (see “4 Autonomous mobility” in Figure 4).

The impact on the automotive industry and more generally on our society will differ by scenario, with the autonomous mobility scenario potentially changing everything.

Figure 4 - Main Scenario Characteristics  The table shows the characteristics of every element of each scenario.

The table shows the characteristics of every element of each scenario.

Impact on the automotive industry

In a business-as-usual scenario, global vehicle production would keep growing and the new vehicle population by 2030/2035 would be similar to the one of today, though xEVs (all electric powered vehicles) would become more important.

In a fully autonomous world, consumers would increasingly buy mobility kilometers or services instead of vehicles, and large fleet owners would emerge (i.e. robocabs companies). People would rely on fully autonomous robocabs that would have gradually replaced owned vehicles in 15-20 years. Furthermore, higher per-vehicle usage rates of robocabs would potentially drive new vehicle production substantially below 2015 levels (up to 30% less), with a much higher share of electrified powertrains (100% of robocabs would be electric) and more advanced self-driving capabilities.

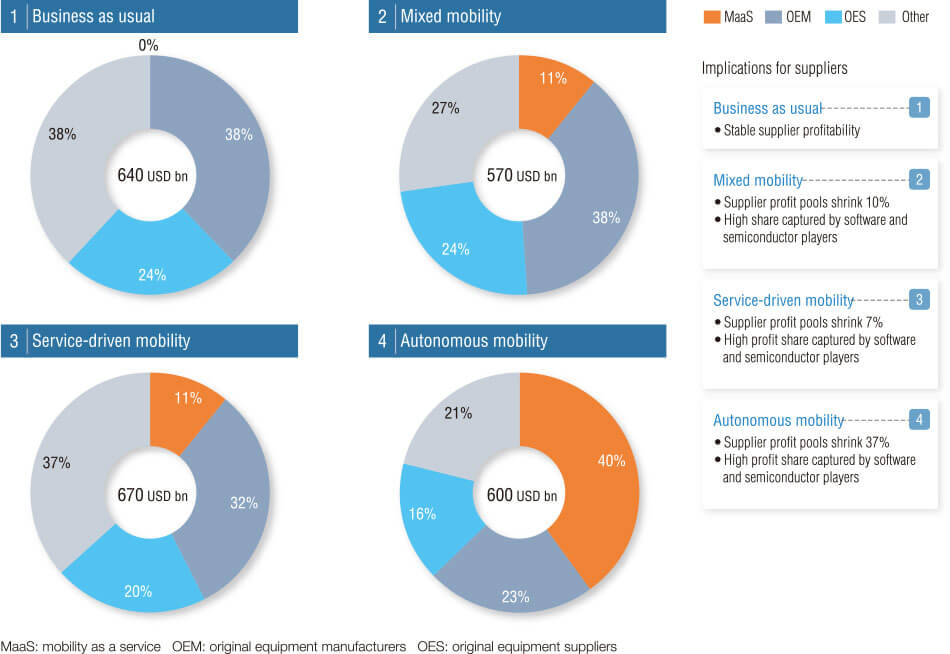

A large amount of business centered around ownership and ownership-like models will be transacted in the future through mobility providers. Rental car businesses, peer-to-peer mobility schemes, and car sharing could be replaced by new service offerings, with a wide range of individualized options tailored to meet diverse conceivable mobility needs. In this context, we expect dramatic changes also in the revenue and profit pools for automotive OEMs and suppliers. Although total profits are expected to increase until 2030 and cars will still be manufactured and sold by OEMs and original equipment suppliers (OESs), mobility services (robocab companies) are likely to earn the biggest share of the future profit pool. The OEM's and OES's shares of total revenues and profits would decrease. The same is true for independent retail, aftersales, and financial services (see Figure 5).

Figure 5 - Profit Pool Implications 2030 [USD bn, Share by Group in %]  These are forecasts of the profit pool of each group in each scenario.

These are forecasts of the profit pool of each group in each scenario.

Impact on consumers and society

Such a scenario would not only disrupt the automotive industry but also the life of many individuals and more generally our society as a whole.

Unfortunately, as in many other industries, high automation will mean a reduction in the number of jobs. Though new technologies will also provide opportunities within the personal mobility space, some categories such as taxi, van, and bus drivers will be completely displaced. According to the 2014 US census data, there were more than 4.4 million Americans working as drivers – in some areas of the country nearly 10% of the workforce rely on driving jobs.

But there is also good news: the new mobility ecosystem will provide a lot of benefits such as:

Increased safety by reducing the number of accidents.

Mobility parity, as a lot of users excluded from car usage now (like the poor, kids, elderly, disabled) would suddenly have access to new mobility services. Over and above that, the new system would enable more efficient, affordable transportation alternatives that prevent underprivileged people from being priced out of central urban living areas.

Additional time to either work or relax by reducing the time so far wasted on driving. This enhances productivity – of professionals who can now work while on the road and of parents who can now send their kids to school on their own, as well as giving everybody more time to sleep, watch TV, surf the Internet etc. while on the move.

More livable and people-oriented cities

Huge amounts of parking space can be freed up and, in general, much less space is devoted to cars, leaving more space for parks, bike lanes, and pedestrian areas. With more electrified vehicles on the street, the air gets cleaner and new services to further speed up traffic and simplify life for everyone will evolve: e.g. the car becomes your ‘wallet' by paying with your car at drive-throughs, fuel or charging stations, and parking or tolls. Suburbs become more desirable as the inconvenience of the commute goes away.

Overall, fewer cars on the road, fewer accidents, less wasted energy, and reduced carbon emissions will not only lead to a higher quality of life and comfort for more people, but also to a cleaner planet.

Inner-city goods mobility will experience the greatest disruption

As new technologies emerge and customer expectations continue to evolve, goods transportation is also on the verge of disruption. The growth of e-commerce has become a generational phenomenon with over half of millennials expecting same-day delivery service as a norm.

Meanwhile, the number of people living in cities continues to grow and will reach 81.5% by 2030, with transport infrastructure that has reached its natural limits. At the same time, urban planners want to see livable, green inner cities with little traffic and low emissions. As a consequence, especially in urban logistics, future-oriented solutions are required to counter current challenges.

Three key trends will drive inner-city goods mobility:

Green:

Several cities are already implementing strict regulations, from innovative pricing to no-drive zones for diesel vehicles (e.g. Singapore, Stockholm, Paris, and Amsterdam). In the future, carbon-neutral logistic fleets will form part of an integrated inter-model transport solution where conventional trucks will handle intercity delivery. Logistics hubs beyond city limits and electric vehicles will supply inner-city districts.

Efficient:

Efficiency will be the backbone of any strategy of operators and manufacturers as total cost of ownership (TCO) remains the most significant factor for transport providers. It will be driven by telematics services providing instantaneous information across the full range of transport options, from conventional trucks, to drone, to pedestrians, making intelligent parcels a reality (e.g. adapting the routes to the traffic volumes).

Premium:

Figure 6 - Physical Internet within the City  This shows the vision of the physical internet within the city.

This shows the vision of the physical internet within the city.

Premium will be whatever urban customers regard as exceptional and for which they are willing to pay an above-average price. The most obvious dimension is time, but premium does not necessarily mean “fast”; it could also, for example, mean a delivery arriving precisely when needed, e.g. in the middle of the night, or emission-free.

It is not yet clear who will set the pace within the inner-city transport environment of the future, but we see some parallels with the personal mobility space, where mobility service providers are expected to take the front end to the customer. So commercial vehicle manufacturers, too, might have to do more than just build and sell vehicles in the future.

This will also have an impact on consumers, especially if the physical Internet vision is fully realized (see Figure 6). Physical Internet is an open global logistics system founded on physical, digital, and operational interconnectivity intended to replace current logistical models. This would mean a real revolution as it would reduce logistics costs by increased network efficiency and reduced inventory, reduce emissions, improve delivery comfort, and increase speed and on-schedule delivery.

Smart Mobility:

a sustainable synergy between vehicle, society, and the environment

No doubt both the personal mobility space and the transport logistics environment are in a transition phase which is quite challenging for automotive players. The described four key trends reshaping the industry (mobility, autonomous, digitalization, and electrification) are creating serious threats to their core business, while the traditional investment logic (e.g. volume growth and filling plants to profitability, flexibility, selective presence in emerging markets) doesn't work anymore.

However, such trends also open up new opportunities. They are reshaping our society, with the overall impact being positive, though the issues of potentially losing millions of jobs in the workforce of the automotive industry (the completion of an electric drive requires at least seven times less effort than a traditional one) will need to be carefully addressed.

To survive the disruption, automotive players will have to leave their beaten track and lead the change, and be quick and flexible to adapt. They must address the part of their business that will be disrupted first, and address new customer groups and their needs.

Those who innovate radically and who think ahead today can become the leading players of tomorrow. According to the motto: lead and adapt or go under.