Blockchains are gaining attention as a new platform technology for financial transactions, offering the benefits of lower intermediation costs with more transaction impartiality and transparency. Their use as a financial transaction platform has the possibility not only to bring about changes in the business models of existing financial services, but also to create new financial services and businesses. This article discusses the technical features of blockchain technology and its potential applications in the finance sector. It also looks at the ways of linking blockchain technology with the IoT and other industries to create new services and businesses, and examines the challenges to be overcome upon achieving them. Hitachi aims to overcome these challenges to pioneer new services and businesses through collaborative creation with customers.

Customer Co-creation Project, Global Center for Social Innovation – Tokyo, Research & Development Group, Hitachi, Ltd. He is currently engaged in the Customer Co-creation Project in the financial and public services fields. Mr. Nagano is a member of the Institute of Electrical Engineers of Japan (IEEJ).

Service Design Research Department, Global Center for Social Innovation – Tokyo, Research & Development Group, Hitachi, Ltd. She is currently engaged in ethnographic research and service design. Ms. Hara is a member of the Japanese Society for Cognitive Psychology (JSCP) and the Human Interface Society.

Digital Platform Solution Laboratory, Research & Development Department, Hitachi America, Ltd. He is currently engaged in the development of blockchain technology for enterprise systems. Mr. Oshima is a member of the Information Processing Society of Japan (IPSJ).

2nd Research Department, Financial Strategy Research Group, Hitachi Research Institute. He is currently engaged in the research of FinTech, blockchain, and IoT trends.

Financial Innovation Center, Financial Information Systems Sales Management Division, Financial Institutions Business Unit, Hitachi, Ltd. He is currently engaged in business planning and development for the financial industry.

BOOSTED by the popularization of smartphones and social media, and by advances in technologies such as big data analysis, financial technology (FinTech) is gaining momentum in the finance sector for its ability to redefine financial services from the end user's perspective. FinTech is used to provide a wide variety of services spanning areas such as payment, personal financial management (PFM), financing, and asset management, and among those services is blockchain. Blockchain is used as a platform technology for Bitcoin*(1) and has been gaining attention as a technology with the potential to replace the financial infrastructure used for transactions such as international remittances. The potential uses of blockchain technology in various applications outside of the finance sector are also attracting interest. Financial institutions have responded to the rise of blockchain technology by starting various forms of demonstration tests to assess its potential.

This article describes the technical features of blockchain technology, the potential applications for it in the finance sector, and also the potential for new financial services and businesses, including those that link with the Internet of Things (IoT) and other industries.

A blockchain is a distributed transaction recording technology that lets multiple network nodes share the transaction records of transactions such as remittances, thereby eliminating the need for a designated organization serving as the transaction intermediary or central manager of transaction records. Blockchains are composed of the following three technology components:

The technologies above prevent falsification of transaction details and duplicate transactions, enabling autonomous transaction record operations without the need for a designated administrator. A typical use case that can be achieved by taking advantage of this feature is remittances using a virtual currency such as Bitcoin. Conventional remittance transactions are done by rewriting the ledger that centrally manages the payer's balance information. International remittances and other transactions that involve multiple intermediary financial institutions or systems incur several intermediary commissions. In contrast, transactions using blockchains enable low-cost remittances by recording value transfers in the transaction records shared by the participants.

The benefits of blockchains for financial transactions and operations are listed below.

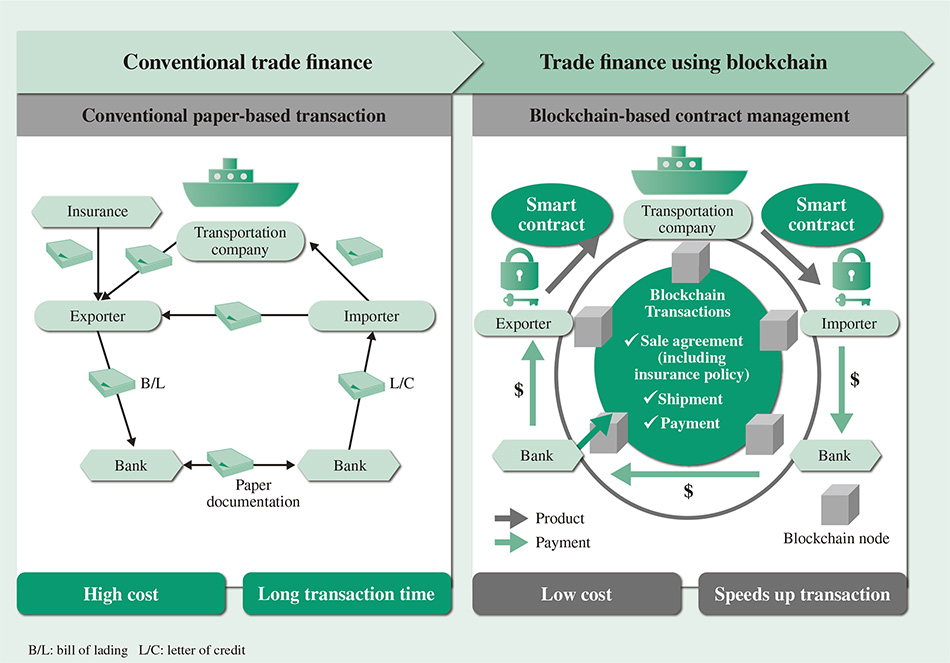

Trade finance provides one example of a use case that takes advantage of blockchain features. In a conventional trade transaction, the bank assumes the credit risk of the importer and exporter and intermediates the account settlement process to ensure that the exporter receives payment and the importer receives delivery (see Fig. 1). But the processes from the signing of the sale agreement to shipment and account settlement are done manually using paper documentation, creating the problems of high administrative workload and long processing time. Using a blockchain for this transaction enables it to be processed impartially as specified in the sale agreement, and speeds up the transaction by letting the stakeholders share transaction statuses in realtime.

Fig. 1—Trade Finance that Takes Advantage of Blockchain Features.

Using blockchains to record trade finance transactions can improve transaction impartiality and speed.

Using blockchains to record trade finance transactions can improve transaction impartiality and speed.

The trade finance use case illustrates how smart contracts enable the impartial execution of transactions, which can significantly reduce the bank's operation costs and lower its liability risk. These benefits enable banks to focus on services that have higher added value, such as new financial services driven by transaction histories stored in blockchains. In this way, blockchains have the potential to bring about reforms in the business models of existing financial services.

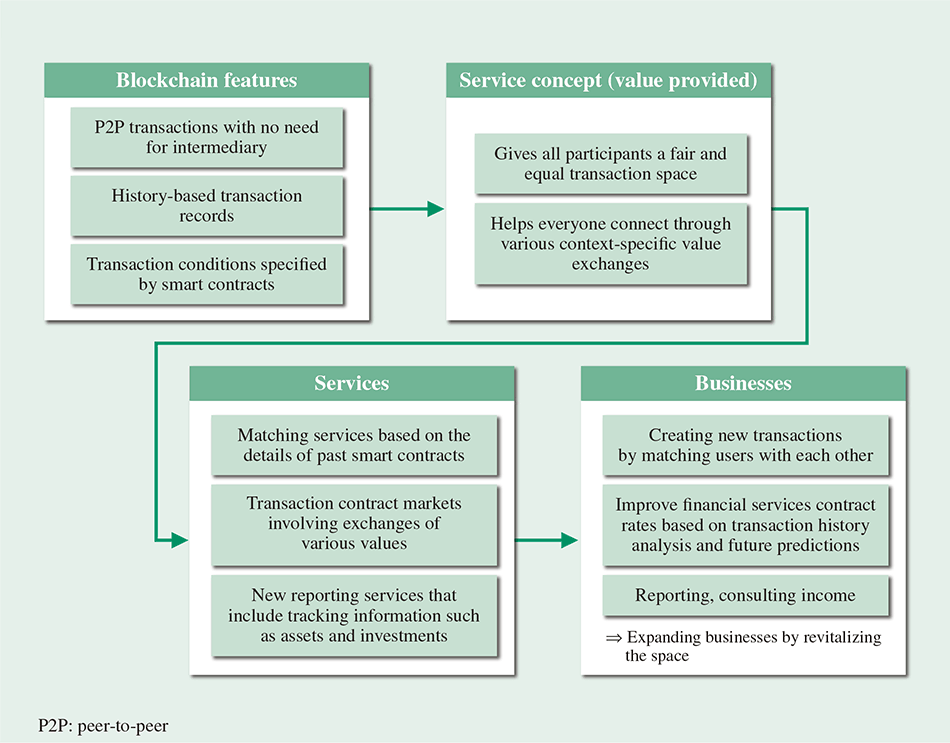

Unlike conventional financial infrastructure such as bank ledger systems, blockchains are a peer-to-peer (P2P) transaction platform driven by transaction history information. This feature can be used to create services and business models based on a new concept, unlike any of the conventional services provided with today's bank accounts (see Fig. 2).

Below are some examples of the wide range of services that could be made possible by a service concept that provides a transaction community enabling equal participation by everyone, and helps them connect through various value exchanges driven by smart contracts that participants can customize themselves.

These services will enable the revitalization of communities and the harnessing of new transactions to further expand business growth.

Thus, by creating a service concept that draws on the features of blockchains to change how consumers and businesses approach financial behaviors, it will become possible to create unprecedented new services and business areas.

Fig. 2—Creating Blockchain-driven Financial Services and Businesses.

Creating a service concept that draws on blockchain features will enable the creation of new financial services unlike anything previously available.

Creating a service concept that draws on blockchain features will enable the creation of new financial services unlike anything previously available.

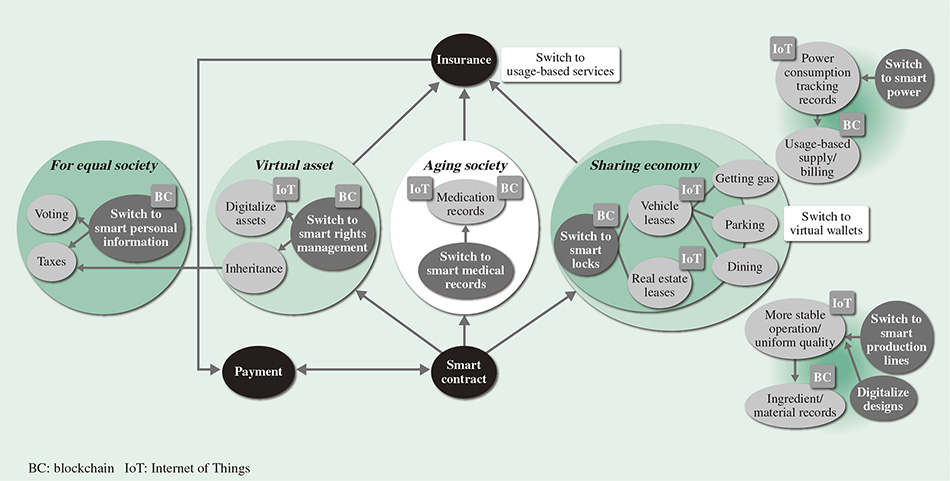

The services and businesses discussed above could be further expanded by coordinating them with the IoT, which interconnects devices using IT. For example, the non-life insurance industry could improve the impartiality and efficiency of policy management and claims payment processes by using blockchains to record insurance policies and using the IoT to monitor those policy provisions. There could also be use cases in which a network-connected device is enabled based on an insurance policy recorded in a blockchain. So coordinating blockchains and the IoT could enable transactions and events that were previously managed and evaluated individually to be processed more efficiently as more wide-scale transactions. Fig. 3 shows how use cases could be expanded in an industry-coordinated space that includes linking with the IoT.

Fig. 3—Expanding Services through Industry Coordination.

Coordinating with industries such as energy, healthcare, and public-domain records could enable the expansion of various types of services, improving business efficiency and creating new services and businesses.

Coordinating with industries such as energy, healthcare, and public-domain records could enable the expansion of various types of services, improving business efficiency and creating new services and businesses.

Some of the challenges that will need to be overcome to create new blockchain-driven financial services and businesses are described below.

Firstly, there are technical challenges. Implementing proper access controls and hiding transaction details are mandatory requirements when using blockchains for financial transactions. Some use cases also will need performance and reliability improvements.

Secondly, there are clerical and systematic challenges. While blockchains enable impartial execution of the trade finance processes described in the second chapter, various exceptional processes such as revising contract details and handling discrepancies can arise in actual practice. How to deal with these processes using blockchains and peripheral processes will need to be studied. Financial transactions are also governed by various laws and regulations and industry standards, which blockchains will need to accommodate in order to match the transaction features.

Thirdly, there are challenges in coordinating with peripheral systems. Blockchains are basically a transaction-recording technology, and do not provide the matching functions provided by securities exchanges, or the netting functions provided by the Bank of Japan Financial Network System (BOJ-NET) (the financial system network operated by the Bank of Japan). Since blockchains alone will not be able to replace every financial infrastructure function, the division of blockchain functions and related functions will need to be organized, and the overall architecture will need to be designed. ID management technology used to uniquely define each item on a blockchain will also be needed for coordinating with the IoT. The method used for coordinating with other systems and blockchains will be another challenge for industry coordination.

Furthermore, new challenges may also arise from the user's perspective. For example, if blockchain-based P2P transactions become commonplace, contracts will be executed between individuals in the manner of smart contracts, which may increase the workload done by individuals. Blockchain acceptance could also start to change as users start to feel uneasy about how the technology accumulates and stores various transaction history records and connections to other users. Technologies and services that accommodate such a change in values will need to be studied.

This article has discussed the features of blockchains and looked at how the technology could be used to create new financial services and businesses in the finance sector. While blockchains could be used to create new financial services and businesses driven by a concept unlike anything previously available, the technology still faces the various challenges described in the previous chapter.

Through collaborative creation with customers, Hitachi aims to concretize the potential use cases of blockchains and to pioneer new services and businesses by overcoming the various challenges facing the technology.