GLOBAL INNOVATION REPORT

Against a background of successive natural disasters and terror threats around the world, a steady supply of electricity including measures against power outages is a common social issue for all countries, from the viewpoint of the safety and security of their residents.

As the introduction of renewable energy proceeds as a measure against global warming, microgrids are looked to as a promising solution to various issues. However, diverse expertise is required for their construction and operation.

Hitachi has newly created a team with such expertise, and through dialogue with many customers is taking on the challenge of developing the North American microgrid market, an advanced arena in the energy field.

In this article, Alireza Aram, who has extensive experience in the energy field, reports on the latest trends in the US market.

Microgrids are one of many distributed energy resource (DER) solutions that are part of a transformation occurring in the US power sector. The power sector is moving from a centralized system to a distributed system. New technologies, supported by regulatory changes, are giving customers more choice and flexibility about their energy supply, management, and costs and enhanced reliability.

A microgrid is the most technically sophisticated of the DER solutions available on the market today. The US Department of Energy defines a microgrid as “a group of interconnected loads and distributed energy resources within clearly defined electrical boundaries that acts as a single controllable entity with respect to the grid. A microgrid can connect and disconnect from the grid to enable it to operate in both grid-connected and island mode.” In the most common configuration, the DERs in a microgrid include the following: solar photovoltaic (PV) systems; combined heat and power units; advanced batteries; and building load control. These systems are actively managed by a microgrid controller that adapts to changing loads and generation operational characteristics. Most of the time, microgrids operate in parallel with the utility grid but also have the unique feature of being able to operate independently of the main utility grid (island mode) in the event of a power outage. As dependence on technology has grown in all facets of society, tolerance for power outages has decreased markedly while at the same time in the USA, vulnerability to power outages has increased due to aging of the grid infrastructure and cyber and physical threats.

This makes the ability to seamlessly “island” from the utility grid in the event of a power outage a key driver for many customers to consider a microgrid versus other less sophisticated DER solutions. Additional customer benefits include reduced energy costs, less volatile energy costs, and reduced emissions.

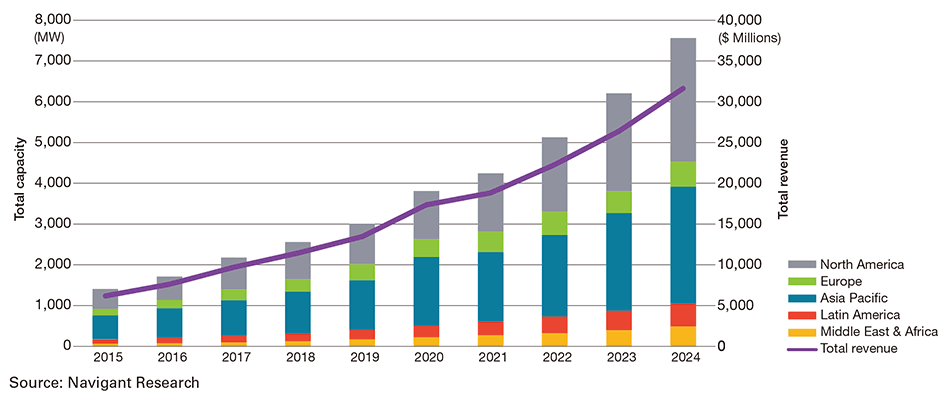

Figure 1Total Microgrid Capacity and Revenue by Region, World Markets: 2015-2024

As seen in Figure 1, microgrids are a global phenomenon. Asia Pacific will be the dominant region with 41.3% of total microgrid revenue. North America is projected to represent 32.5% of global market share. Cumulative revenue (calculating total microgrid asset value) is expected to be $164.8 billion by 2024.

Data from Navigant Research show that the current installed base of microgrids in the USA prior to 2015 was slightly over 1,000 MW. From January 2015 to June 2016, 71 microgrids have been installed (~592 MW) with an estimated value of $1.7 billion (USD).

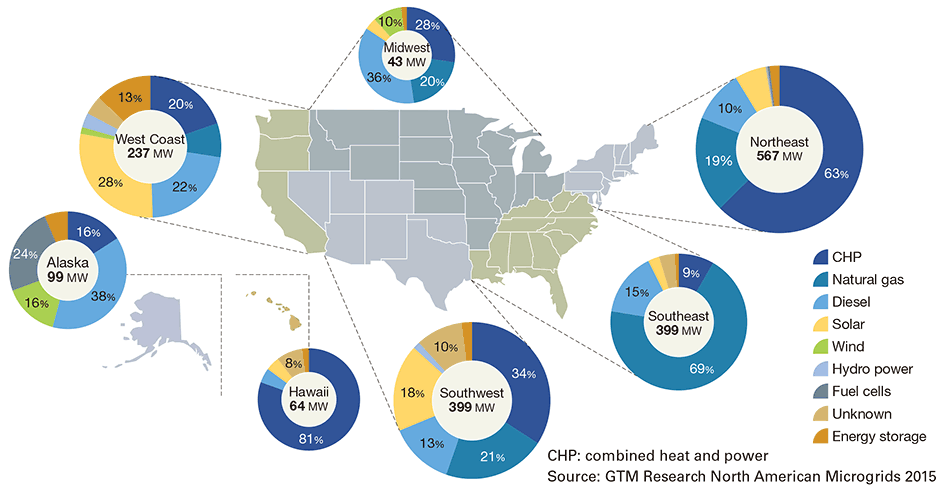

GTM Research has analyzed microgrid deployments in the USA as shown in Figure 2, which depicts regional concentrations as well as generation sources. Geographic drivers are high utility prices, regulatory incentives, and greater vulnerability to grid outages.

Increased resilience underpins many of the current state-level programs supporting microgrid adoption in several US States.

While resilience was the initial driver for much of the current state-level policy support, regulators are starting to expand their view of the benefits microgrids can provide to society as it becomes clearer that they are one of a suite of DER solutions available to utilities to achieve a variety of goals, including

Figure 2Microgrid Deployments in the USA

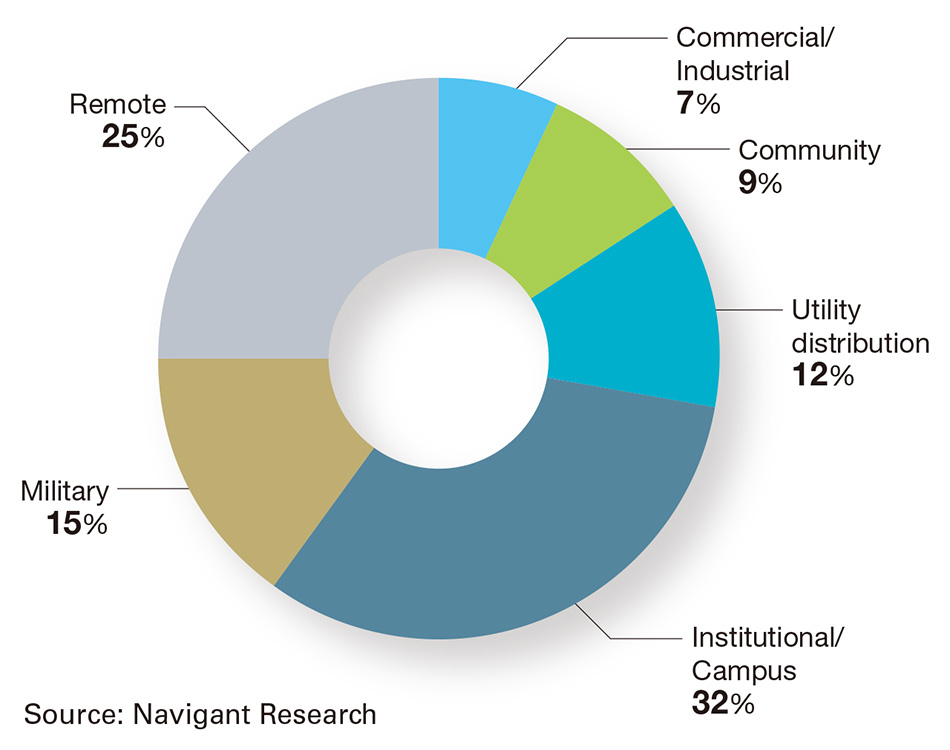

Figure 3Applications for Microgrids

Customer applications for microgrids are wide ranging, from providing power for mission-critical functions in cities and at military bases to providing greener, more reliable energy to universities and commercial industrial sites (see Figure 3).

The commercial and industrial (C&I) segment has been slowest to gain traction due to challenges in the value proposition related to return on investment and customer reluctance to evaluate alternatives to traditional backup generation or redundant utility feeds. However, new vendor business models which enable customer adoption without capital expenditure through power purchase agreements (PPAs) are driving an increase in C&I adoption. An increasingly important consideration for C&I customers in North America is the fact that microgrids can provide indefinite power supply in a prolonged grid outage whereas backup generators are dependent on fuel delivery, which can be difficult during major weather events.

North America leads all other regions of the world in terms of annual capacity and revenue in this customer segment. Total capacity in 2015 was 219.7 MW and is expected to grow to almost 1.2 GW annually by 2024 with annual revenue for this segment in North America expected to reach $4.2 billion by 2024. College/ university campuses are particularly attractive microgrid candidates due to their large electric and heating loads. Further, they frequently have their own electric and thermal infrastructure and typically have only a few points of interconnection to the utility, making projects technically easier and less expensive. Universities have found that maintaining power supply during a grid outage is an important point for many fee-paying parents in the USA. Further, the ability for microgrids to help address the aggressive sustainability targets that many colleges/universities have adopted as well as using the microgrids as a research and educational platforms are important considerations. Example microgrids include those at the University of California, San Diego; New York University; Fairfield University; and Princeton University.

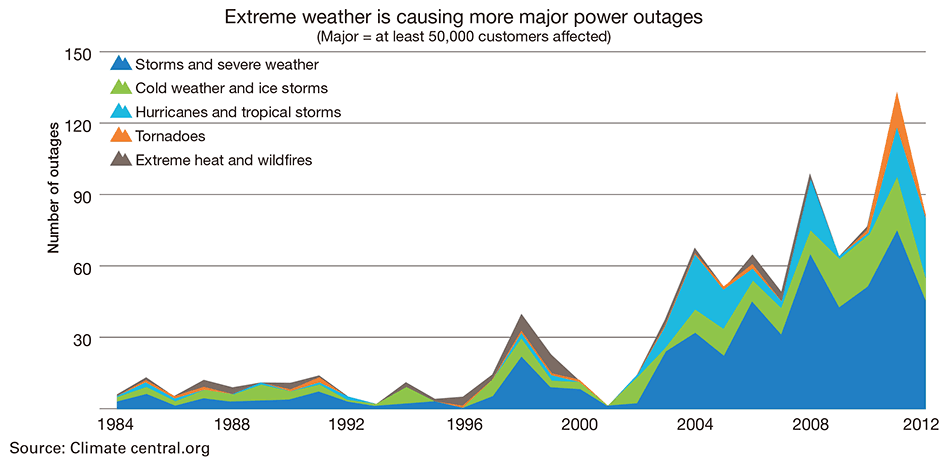

State-sponsored microgrid programs have raised awareness of microgrids as viable solution for addressing community resilience goals. Community microgrids typically focus on providing energy resilience for critical facilities in the aftermath of a major storm. Increases in the magnitude and frequency of hurricanes and ice storms in the eastern USA have resulted in communities being without power for many days at a time (see Figure 4). In many locations, it is difficult for residents to evacuate. Microgrids allow residents to shelter in place and still have major services available to them, such as police, fire, medical, pharmacy, shelter, gasoline, and food. Many cities are considering microgrids to ensure continuity of critical municipal services. A single municipal customer is more straightforward than community microgrids, which involve multiple participants and off-takers (hospitals, city hall, fire stations, grocery stores, etc.). These microgrids are the most challenging from a technical, business model, and financing standpoint. However, regulators in many states appear determined to break down these barriers. The New York Prize Program, for example, funded 83 community microgrid design and feasibility studies. Hitachi received 12 of these awards and delivered feasibility studies to its partner communities in June/July 2016.

Figure 4Power Outages Caused by Major Weather Events

The US military has an initiative, Smart Power Infrastructure Demonstration for Energy Reliability and Security (SPIDERS). The program aims to apply microgrids to provide power to mission critical facilities in the event of a loss of the utility grid or attack. One of the attributes of the solution is to integrate solar PV and energy storage to the existing diesel backup generators to provide a portfolio of diverse fuel sources, enabling a longer duration solution and lower carbon footprint than traditional backup generators. There have been several demonstration projects so far.

Utilities are exploring the role of microgrids as an infrastructure and operational resource and as a potential new revenue stream making them a potential Hitachi customer or maybe a competitor. As an infrastructure resource, microgrids can support many operational goals and challenges the distribution utilities currently face. Several utilities with non-regulated businesses have entered the microgrid business to serve existing customers. Utility microgrid projects include San Diego Gas & Electric’s Borrego Springs Microgrid, Duke Energy’s Mount Holly Microgrid, and National Grid’s Potsdam Microgrid.

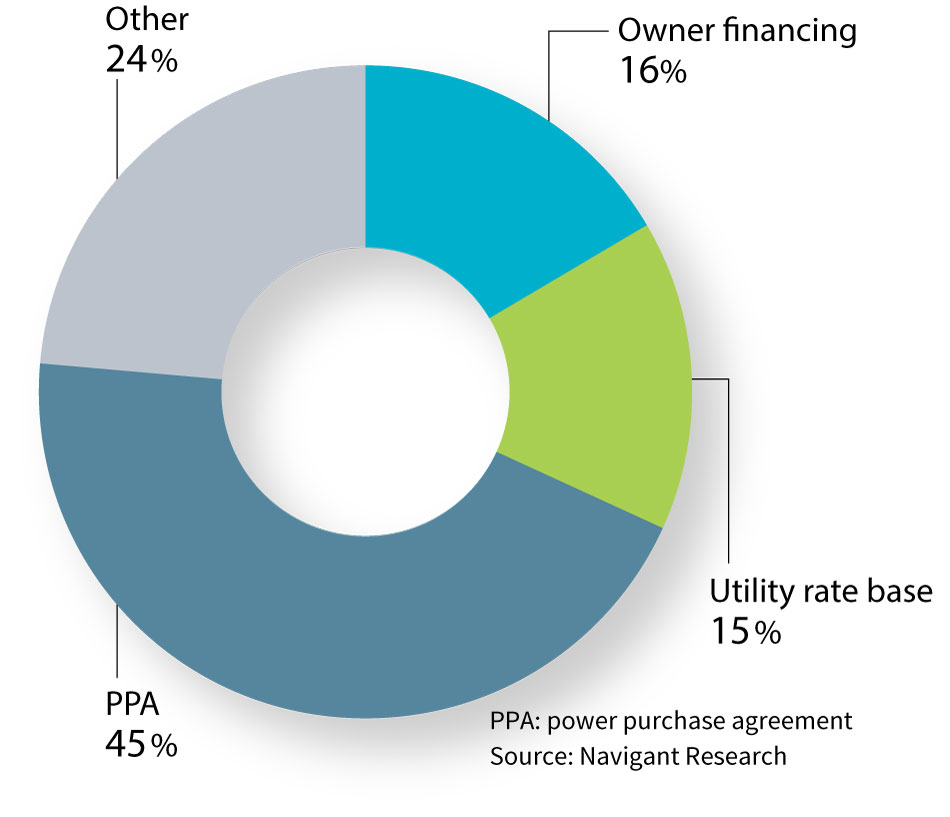

Figure 5Non-military Microgrid Ownership by Capacity

Microgrid projects are complex. They require strong expertise in technology selection, financing solutions, local codes and regulations, utility requirements, and customer procurement policies. Hitachi has assembled a team in Hitachi America’s Energy Solutions Division that has the experience to address all facets of microgrid project development, engineering, financing, construction, and operations in order to provide turnkey microgrid projects to the US market.

Figure 5 depicts the various ways in which microgrids are currently paid for in the USA.

The Power Purchase Agreement is expected to increase over time as C&I and other customer segments demand a ‘microgrid as a service’ offering from vendors. To effectively compete in the market, Hitachi has developed a business model that is similar to the PPA model, namely, an energy services agreement (ESA), which includes electric and heat energy. The ESA is an agreement for energy and services between a project owner [in the legal form of a special-purpose entity (SPE)] and the customer. The SPE can be funded through one or more investors who then contract with Hitachi’s Energy Solutions Division for engineering, construction, and operations services.

Hitachi America’s Energy Solutions Division is aggressively pursuing the North American microgrid market as a one-stop service provider that can deliver a turnkey microgrid and then operate and maintain the system over the lifetime of the system. The market is currently emerging and projected for significant growth in the next 10 years, making this a promising business opportunity to establish Hitachi as a market leader in this industry.