25 December 2020

Huijuan Shao

R&D Division, Hitachi America, Ltd.

Equipment-as-a-service (EaaS) is gaining popularity in industries as it provides the customers with high flexibility and scalability and allows a service provider to optimize operations so that both the service provider and the customers benefit. The pricing modeling, however, is a key challenge in EaaS due to a change in the business objectives from selling products to providing services. In particular, EaaS can face severe high-cost issues as unexpected equipment failures can result in expensive downtime costs. My colleagues and I built a hybrid model that balances the costs and benefits of EaaS by using failure prediction (FP) in the predictive maintenance (PdM) domain and dynamic pricing.

We started by building a gradient boosting (GB) based FP model to predict failure probabilities. Then a risk-based dynamic pricing (RBDP) model was applied to a confusion matrix of the FP to estimate the cost effects of predicted failures with a constrained objective function. Finally, the FP model and the RBDP model were trained simultaneously to minimize the objective function so that it compensates for failure costs and maximizes overall profit gain. The proposed hybrid modeling approach was compared to a traditional FP without a pricing policy approach and an FP with a static pricing policy approach, and indicated a significant improvement in in profits.

In FP settings, four different approaches have been commonly used to solve binary classification problems in predictive maintenance: support-vector machine (SVM), gradient boosting (GB), neural networks, and random forest [1] [2] [3] [4] [5]. We used GB as it shows a generally higher performance in experiments.

Let me introduce our approach by showing how it solves a case in which both FP and pricing policy are considered to make optimal decisions. The price decision making happens at the beginning of a lease when a brand new or used equipment can be leased out. To make it more general, we assumed that the new equipment is given to the customers for the first lease and after that, customers can choose to continue with the (used) equipment or lease new ones at each point of renewal time. In our research, we considered the more challenging case of renewal contract pricing. The question tackled was: At a lease renewal point, what prices shall a company provide to customers so that it can achieve a maximum overall profit, given that equipment failures may happen in the renewal contract period?

To answer this question, we first compared the architecture of our proposed approach with previous works. Then we introduced two different types of models: 1) a naive dynamic pricing model that combines binary failure predictions with simple failure costs; 2) a second model that not only considers failure predictions and costs, but also penalties to constrain dynamic pricing policies to make it more realistic to real-world scenarios.

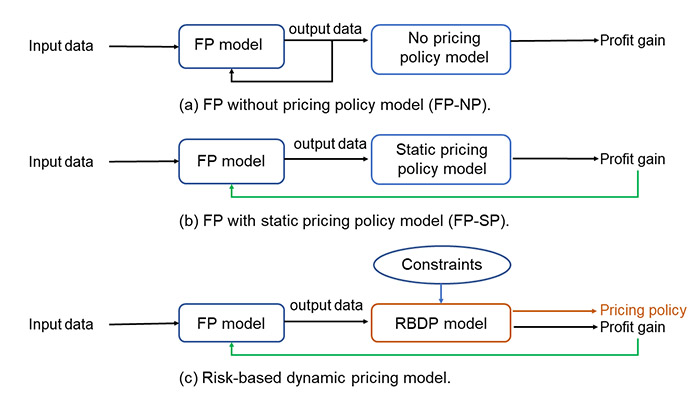

Figure 1: Combing failure prediction with pricing models

Figure 1 illustrates three combinations by combing failure prediction with pricing models. (a) describes the traditional approaches which optimize metrics such as F1–score to select the best FP model without optimizing the pricing strategy (i.e., using existing pricing strategy). (b) illustrates a cost-based learning approach [6] which optimizes the total profit gain with the cost impact modeled and generates an optimized static pricing policy. (c) proposes a hybrid model which combines FP and RBDP to recommend a dynamic pricing policy under constraints.

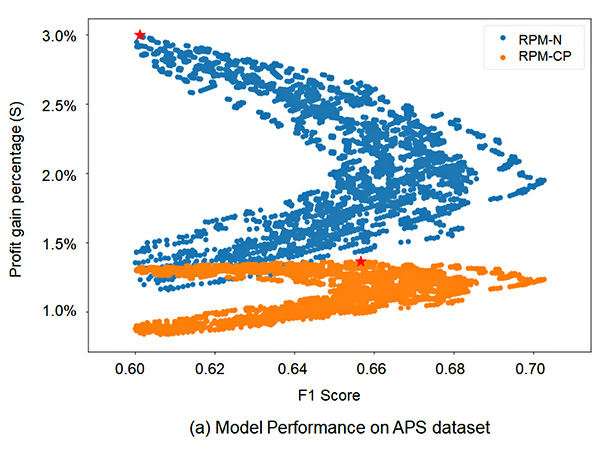

We conducted experiments on two datasets, i.e. Air Pressure Systems (APS) failure data for Scania Trucks and NASA Commercial Modular Aero-Propulsion System Simulation (C-MAPPS) dataset.

Figure 2: F1 score and profit gain percentage S. The highest S is indicated by red stars

Figure 2 shows the results. It was observed that the highest F1 score cannot guarantee the highest profit gain S. For example, RPM-CP model achieves the best S at somewhere slightly lower than the best F1 score. A plausible explanation is that with appropriate pricing policy found by the dynamic pricing model, it is possible to gain more by offering a reasonably lower price for non-fail assets to keep the customers while compensate the loss by offering higher prices for a new asset or a to-fail asset.

To the best of our knowledge, this is the first work formulating the pricing problem based on PdM and comprehensively train a hybrid model. We demonstrated the effectiveness of our method on two well-known benchmark data sets, and showed that the method can obtain an improvement of 3.75% in terms of profit gains compared with the most widely adopted baseline (FP-NP) in industry. For more detailed information, we suggest that you read our full paper which can be found at https://ieeexplore.ieee.org/abstract/document/8999183 [7].

Many thanks to my co-authors Chi Zhang, Chetan Gupta, Seiji Joichi, and Ahmed Farahat with whom this research work was jointly executed.